The digital marketplace is currently undergoing a fundamental structural shift as major technology platforms attempt to transition from being mere discovery engines to becoming the final destination for commercial transactions. Tech giants including Google, Meta, and ByteDance have integrated native checkout features into their ecosystems, while OpenAI’s ChatGPT has begun offering direct purchasing capabilities, bypassing traditional brand websites entirely. However, a recent comprehensive survey of digitally fluent shoppers suggests that despite the billions of dollars invested in "in-platform" commerce, consumer trust remains firmly anchored in the direct-to-consumer (DTC) brand website.

The data indicates a significant disconnect between the technological capabilities of platforms and consumer willingness to utilize them. While the infrastructure for a seamless "discovery-to-delivery" pipeline exists, shoppers are expressing deep-seated reservations regarding security, authenticity, and the ethics of algorithmic influence. As platforms attempt to consolidate the entire shopping journey, brands are left questioning the future utility of their independent web presence. The findings of this study suggest that the brand website is not merely a logistical necessity but a critical sanctuary of trust in an increasingly opaque digital environment.

The Evolution of In-Platform Commerce: A Brief Chronology

To understand the current tension between platforms and brand websites, it is essential to trace the evolution of digital shopping over the last two decades. The transition from search-based discovery to integrated commerce has occurred in several distinct phases.

The early 2000s marked the era of "Search and Redirect." In 2002, Google launched Froogle (later Google Shopping), which functioned as a comparison engine that directed users to external merchant sites. For nearly fifteen years, this remained the standard model: platforms were the "top of the funnel," and brand websites were the "bottom of the funnel."

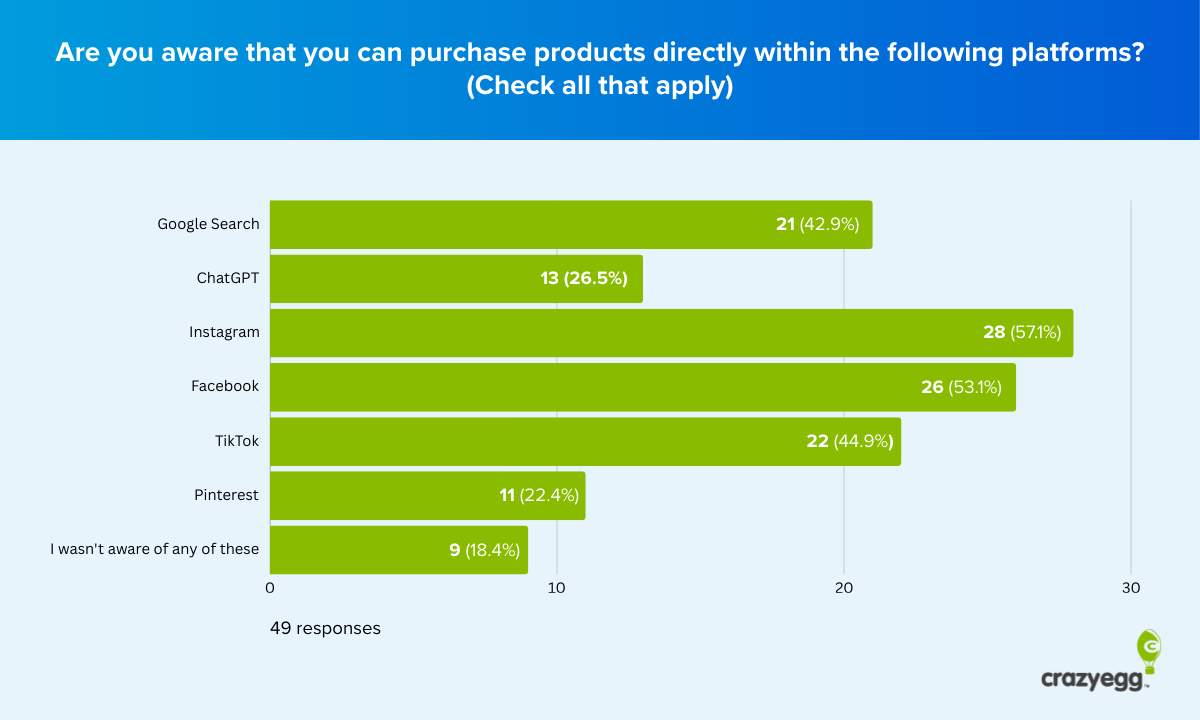

The mid-2010s saw the rise of social discovery. Platforms like Instagram and Pinterest became visual catalogs, but the transaction still required an exit from the app. The "Integrated Era" began in earnest around 2019, when Instagram introduced native checkout, allowing users to buy products without leaving the application. This was followed by the rapid expansion of TikTok Shop in 2023, which utilized a high-velocity video-to-checkout model that had already seen massive success in Asian markets through apps like Douyin.

By 2024, the landscape entered the "AI-Assisted Era." With the integration of search and generative AI, platforms like ChatGPT began experimenting with purchasing agents that can find, recommend, and buy products on behalf of the user. Despite this rapid technological acceleration, the recent survey of 49 high-engagement shoppers reveals that consumer psychology has not kept pace with these structural changes.

Core Findings: The Resilience of the Brand Website

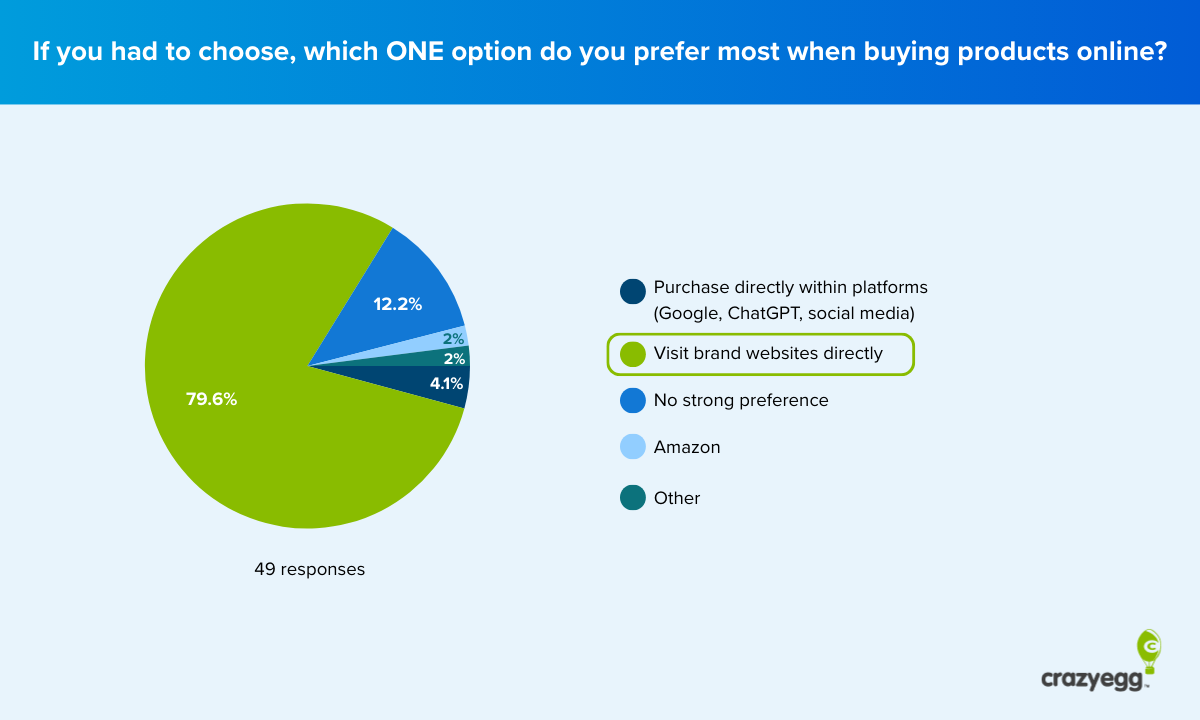

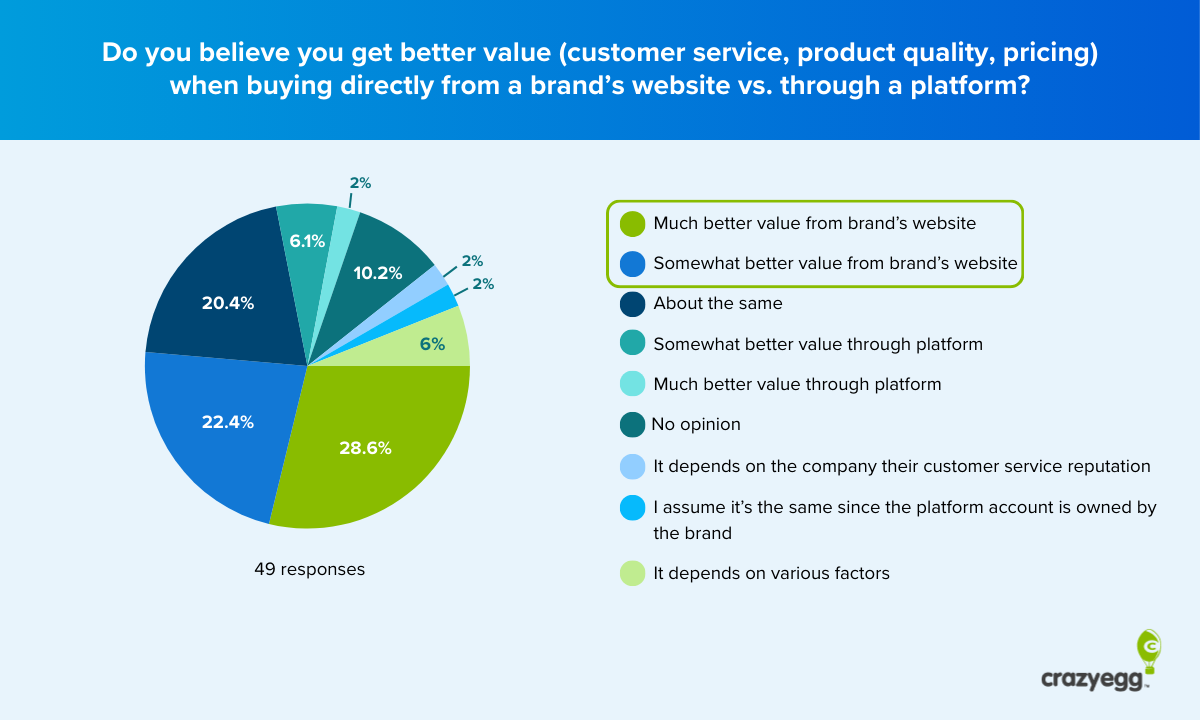

The survey, conducted across a network of digitally active, mid-career professionals, found that 80% of respondents still prefer to complete purchases on a brand’s official website. This preference is not merely a result of habit; it is a deliberate choice driven by a perceived lack of security on third-party platforms. Only 4% of participants indicated a preference for in-platform purchasing, a figure that stands in stark contrast to the aggressive marketing of features like TikTok Shop and Instagram Checkout.

Despite the convenience offered by native checkout, 69% of shoppers reported that their usage of brand websites has remained steady over the past year, while 20% have actually increased their direct visits. This suggests that the "DTC" model is not in decline; rather, it is being reinforced by a growing skepticism of the "middleman" platforms.

The primary drivers for choosing a brand website over a platform are:

- Payment Security: High-profile data breaches and the opaque nature of platform-level data harvesting have made users wary of storing credit card information within social apps.

- Product Authenticity: Shoppers expressed concern that platforms, particularly those with third-party marketplaces, are susceptible to counterfeit goods and "dropshipping" scams.

- Customer Support: The difficulty of managing returns or resolving disputes through a platform intermediary remains a significant deterrent.

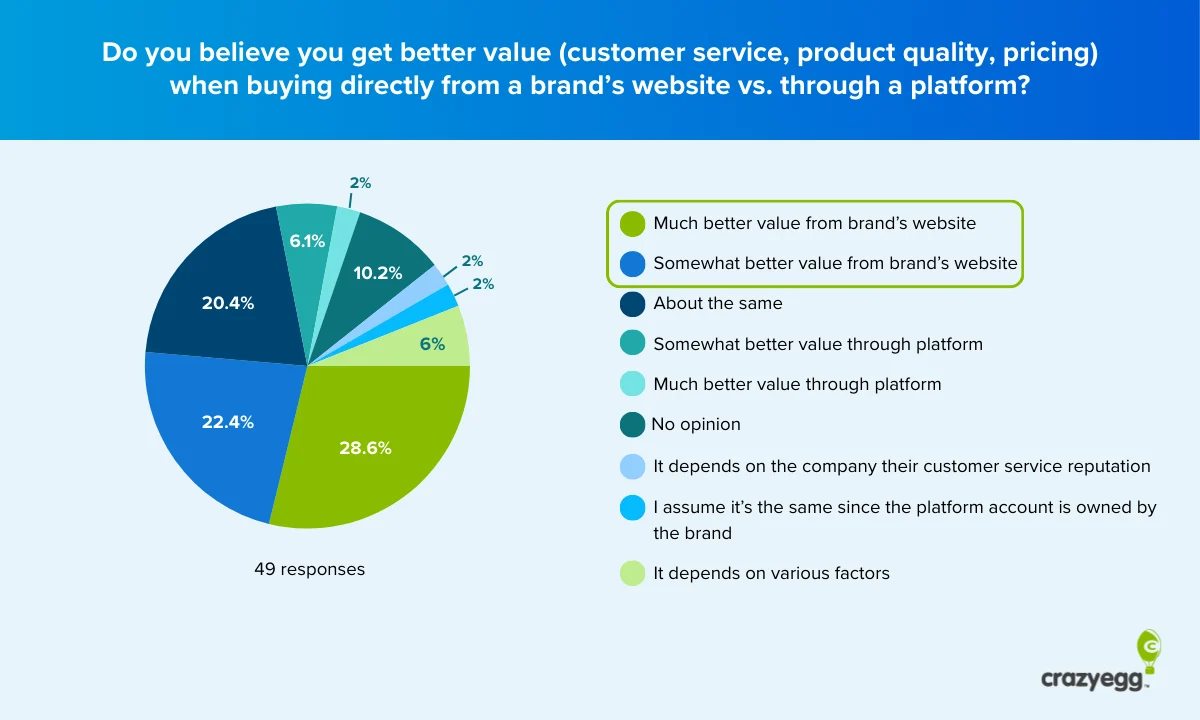

- Brand Connection: 59% of respondents reported feeling a stronger emotional connection to a brand when buying directly, suggesting that the transaction environment is a key component of brand equity.

Demographic Disparities: Gender and Age as Predictors of Behavior

The survey revealed a profound gender divide in how in-platform shopping is perceived and utilized. Women are three times more likely than men to have completed an in-platform purchase (42% vs. 14%). Interestingly, women also represent the group most committed to brand websites, with 92% stating it is their preferred channel. This paradox suggests that for many women, a brand’s official social media page is viewed as a digital extension of the brand itself, rather than a separate third-party platform.

Conversely, men demonstrated a much higher reliance on established marketplaces, specifically Amazon. For 52% of male respondents, Amazon is the default starting point for any purchase. Their resistance to new platform shopping is driven by "The Amazon Default"—a trust in the logistics and return infrastructure of a known entity rather than a rejection of third-party shopping in principle.

Age-based data also challenged conventional wisdom. The 35–44 age group emerged as the most resistant to in-platform shopping, citing ethical concerns and a dislike for "algorithmic manipulation." This cohort expressed a sophisticated understanding of how platforms use data to steer consumer choices, leading to a principled refusal to engage. In contrast, the 45–54 age group showed a surprising openness to platform shopping, with a 40% adoption rate, though they remained highly concerned about the logistical "after-care" of the purchase, such as return policies.

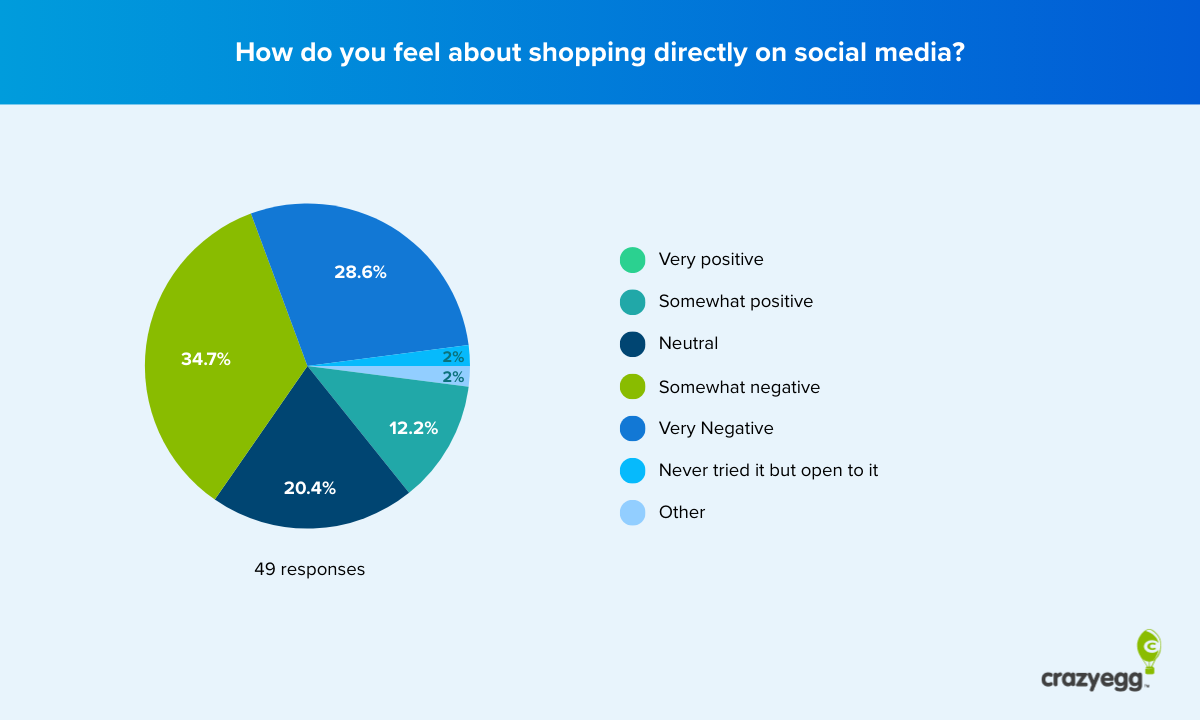

The Credibility Gap in AI and Social Commerce

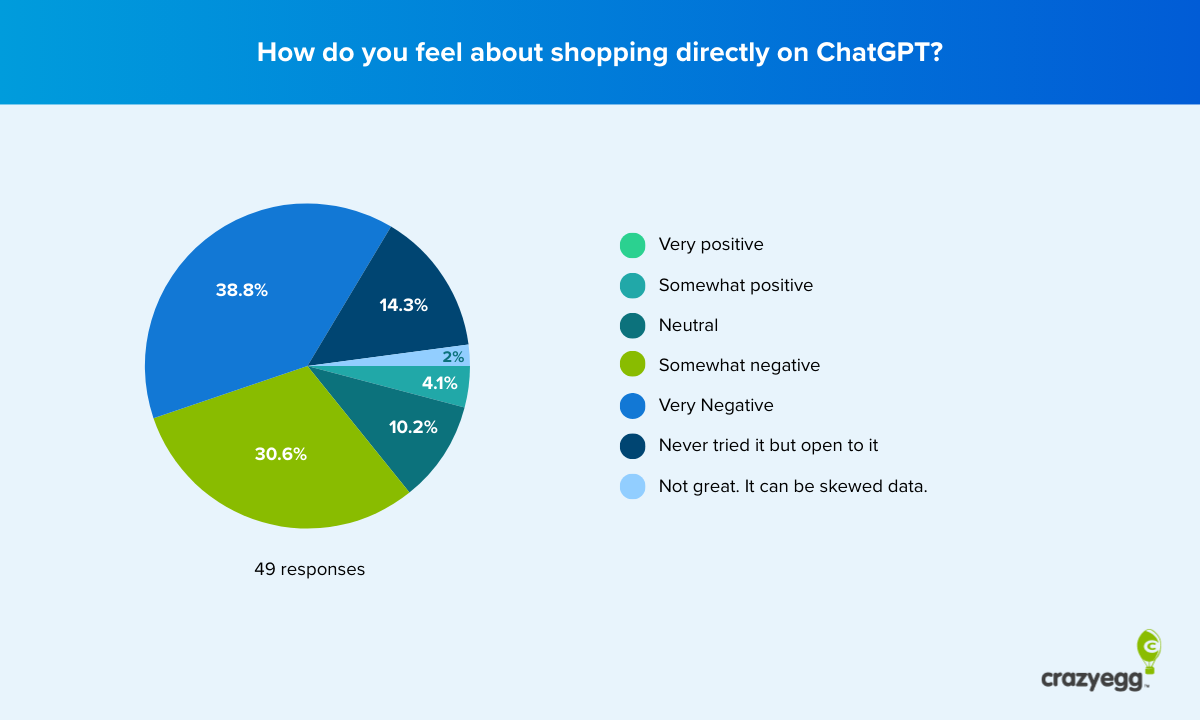

The most significant hurdle for new commerce entrants is the "Credibility Gap." This is most visible in the sentiment toward ChatGPT and other AI-driven shopping tools. 70% of respondents felt negatively about shopping through an AI interface, the highest negativity rating of any platform.

The resistance to AI commerce is not rooted in technophobia; 96% of the survey participants described themselves as tech-savvy. Instead, the resistance is informed by an understanding of how these systems are monetized. Many participants expressed concern that AI recommendations would be "pay-to-play," favoring brands that pay higher commissions rather than those that offer the best quality or value. One respondent noted, "I wouldn’t trust suggestions coming from ChatGPT, as that may likely be swayed by who is paying a higher commission."

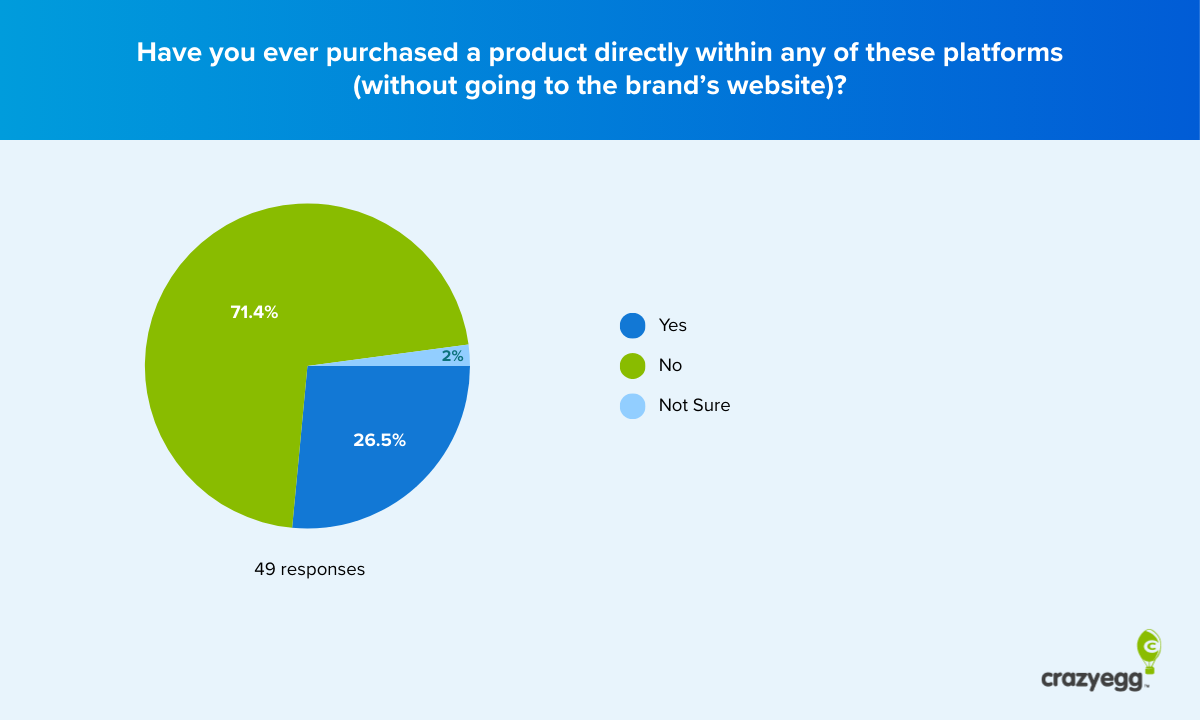

Social media platforms occupy a middle ground. While 64% of participants view social commerce negatively, it is the category with the most potential for movement. The survey found that sentiment often shifts after the first successful purchase. Among those who have never bought in-platform, distrust is high; however, for the 27% who have "crossed the line," the trust gap between platforms and brand websites narrows significantly.

The Amazon Factor and the Marketplace Default

While the study excluded traditional marketplaces like Amazon and eBay to focus on discovery platforms, these incumbents loomed large in the qualitative responses. Amazon is frequently viewed as the "necessary evil" or the "evil I know."

The infrastructure that Amazon spent decades building—one-click ordering, reliable two-day shipping, and a no-questions-asked return policy—serves as the benchmark against which all in-platform shopping is measured. For many shoppers, the decision is not between a brand website and Instagram; it is between a brand website and Amazon. New platforms like TikTok and Google Shopping are not just competing against brand loyalty; they are competing against the logistical certainty that Amazon provides.

Broader Implications for Brands and Platforms

The findings of this survey suggest that the "death of the brand website" has been greatly exaggerated. For brands, the website remains a critical asset for building trust, collecting first-party data, and ensuring a premium customer experience. In an era where platforms are increasingly viewed as "extractive" or "manipulative," the brand website serves as a controlled environment where the relationship between merchant and consumer can be nurtured without the interference of a third-party algorithm.

However, platforms are unlikely to retreat. The shift toward native commerce is a defensive move to capture "attribution"—the ability to prove that an ad led directly to a sale. For platforms to overcome the current resistance, they must address the credibility gap by:

- Standardizing Return Policies: Reducing the friction and risk of post-purchase logistics.

- Increasing Transparency: Being open about why certain products are recommended (organic vs. sponsored).

- Enhancing Verification: Implementing more rigorous vetting for sellers to combat the "scam" perception.

For the modern consumer, the act of purchasing is becoming an ideological statement. The data shows a growing segment of "hard-no" shoppers—individuals who are highly tech-literate but refuse to shop in-platform on principle. These shoppers value privacy and autonomy over the convenience of a "Buy Now" button.

Ultimately, the survey highlights that while technology can make shopping faster, it cannot inherently make it more trustworthy. The brand website continues to win because it represents a direct, transparent transaction. For platforms to truly win the e-commerce war, they will need to prove that they are more than just efficient middlemen; they must prove they are reliable stewards of the consumer’s trust and data. Until then, the "com" will remain the king of the digital economy.