Tuesday, November 18th, 2025 – 1:13 pm

The digital advertising technology landscape is currently a crucible of intense competition and dramatic maneuvering, with underlying financial pressures forcing industry players to redefine their strategies and publicly challenge rivals. For much of the past year, the ecosystem has been a hotbed of conflict, marked by disputes over data access, strategic shifts impacting industry standards, and increasingly sharp rhetoric from key executives. These tensions, once confined to industry forums and executive suites, are now manifesting in tangible ways through company earnings reports and public pronouncements, signaling a significant inflection point for programmatic advertising.

The once-unified front against dominant players like Google has fractured. Companies that once found common ground in navigating the evolving privacy landscape, particularly concerning Google’s Chrome Privacy Sandbox initiatives, now appear to be diverging. The Trade Desk, a major demand-side platform (DSP), has been particularly assertive, employing strategic moves that have elicited strong reactions from supply-side platforms (SSPs) and other ecosystem participants. Open-source initiatives like Prebid and industry governance bodies like the IAB Tech Lab, which aim to foster transparency and interoperability, are finding themselves at the center of these escalating disputes, with their roles and allegiances being scrutinized. This turbulent environment has not gone unnoticed by investors, who are closely examining the financial health and strategic direction of ad tech companies as evidenced by recent quarterly earnings calls.

The Root of the Conflict: Financial Pressures Underpinning Strategic Battles

While debates about data transparency and supply chain roles are frequently cited, the current acrimony in the programmatic space appears to be driven by a more fundamental issue: declining revenue across the board. The third-party programmatic companies, which once saw The Trade Desk as a significant partner and a bulwark against Google’s market power, are now finding themselves at odds with its evolving strategies. This shift in dynamics is becoming increasingly apparent as companies release their financial results.

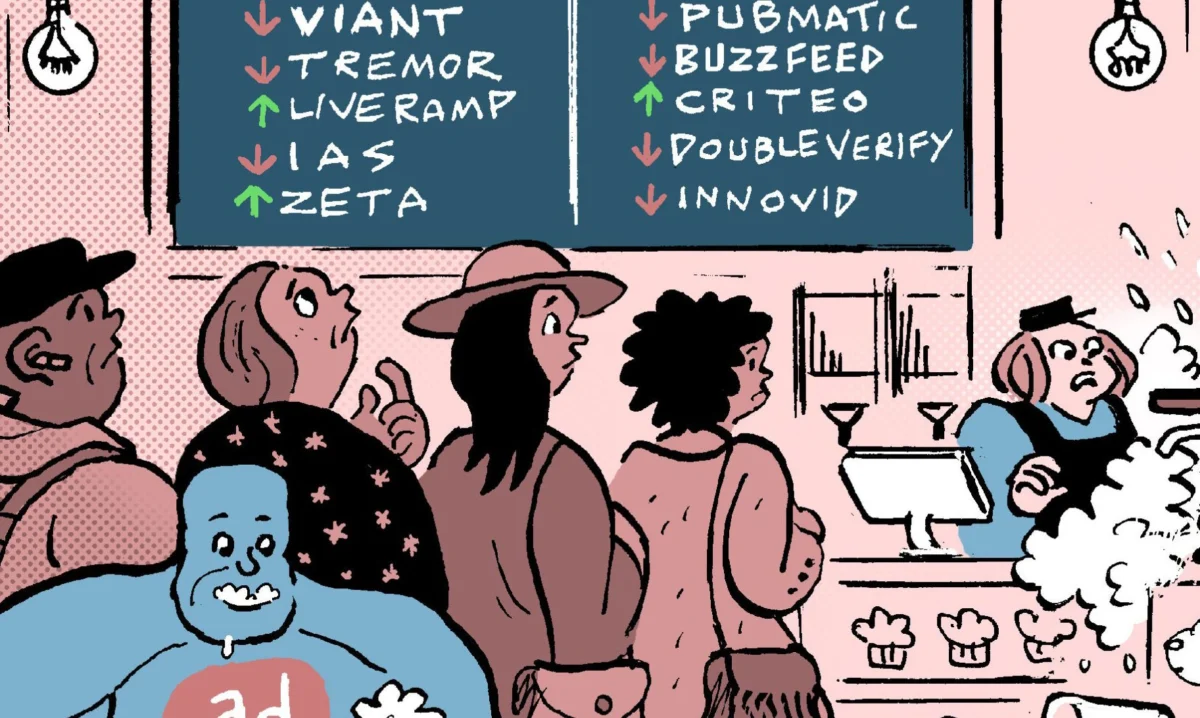

Recent earnings reports from prominent SSPs like Magnite, PubMatic, and Nexxen have revealed a concerning trend: unexpected and significant decreases in spending from unnamed DSPs, or potentially a single dominant DSP, during the third quarter of 2025. This downturn has forced these companies to publicly address the impact on their revenue streams.

Rajeev Goel, CEO of PubMatic, alluded to The Trade Desk’s new ad-buying platform, Kokai, stating that it “operates differently from what we have seen.” This subtle observation echoed earlier sentiments from PubMatic’s leadership regarding a sudden reduction in spend from a particular DSP. Similarly, Michael Barrett, CEO of Magnite, directly identified The Trade Desk as the source of a strategic change that “prioritized OpenPath as a default path for supply.” This move, Barrett explained, necessitated Magnite’s direct engagement with major agency buyers to re-establish a “preferred supply path.” Given The Trade Desk’s significant role as a demand source and Magnite’s position as a major programmatic supply provider, this strategic shift inevitably had a notable impact on Magnite’s business.

Nexxen, which operates both a DSP and an SSP, revised its financial forecast downwards for the remainder of the year. CEO Ofer Druker attributed this revision to a failure to observe the typical surge in growth heading into the holiday season, a pattern that usually begins in October. He clarified that the issue was not isolated to a single DSP but represented a programmatic-wide reduction in spending, a plateau rather than the anticipated pre-holiday acceleration.

The challenges are not solely confined to SSPs. System1 CEO Michael Blend reported that an unnamed programmatic vendor in their demand channel had exposed the company to “significant invalid or nonhuman traffic.” System1 is currently seeking reimbursements and is reportedly considering legal action, highlighting concerns about the quality and legitimacy of traffic within the programmatic ecosystem.

Strategic Positioning and Shifting Narratives in a Competitive Arena

Beyond the immediate financial repercussions, the escalating antagonism is also a strategic play. Companies are actively vying for market position and attempting to shape investor and marketer perceptions of how programmatic advertising should function. This involves crafting narratives that favor their own business models and cast rivals in a less favorable light.

Jeff Green, CEO of The Trade Desk, notably stated to investors that “I don’t think Amazon has a DSP as we define it,” a comment that implicitly draws a distinction between Amazon’s integrated offerings and The Trade Desk’s pure-play DSP model.

In contrast, Tim Vanderhook, CEO of the independent DSP Viant, framed the competitive landscape by stating, “we see less competition when you look at truly objective buy-side-only platforms.” This is a deliberate attempt to categorize competitors and implicitly exclude The Trade Desk, which he characterized as “no longer independent or objective” due to its prioritization of OpenPath supply integrations.

Nexxen’s CEO, Ofer Druker, further elaborated on this trend, noting that “Big DSPs in the future will have to build their own end-to-end solutions in order to increase their margins.” He observed the movement of large DSPs, such as The Trade Desk, onto the supply side of the ad exchange, suggesting a strategic imperative for vertical integration to capture greater value. These divergent perspectives from independent DSPs underscore a fundamental disagreement about the future structure and competitive dynamics of the programmatic ecosystem.

The designation of some SSPs as “resellers” by The Trade Desk has also generated significant concern among investors. Both PubMatic and Magnite have publicly pushed back against this label. PubMatic’s CEO, Rajeev Goel, asserted that “PubMatic is not a reseller” and emphasized the company’s strong partnership with The Trade Desk, downplaying any bitterness over reduced spend or the “reseller noise.” He described the ecosystem as “multifaceted, certainly complex.”

Michael Barrett of Magnite echoed this sentiment, clarifying that while supply-side resellers are a genuine concern, the term does not apply to Magnite. He expressed support for “cleaning up the system” by eliminating duplicate bids and low-quality impressions, reiterating, “Let’s be clear, we don’t believe Magnite is a reseller. I think the term applies to others.” This defensive posture highlights the reputational damage associated with being labeled a reseller, particularly in an environment where transparency and efficiency are paramount.

The Broader Implications: A Restructuring of the Programmatic Ecosystem

The current turmoil in the ad tech industry is not merely a series of isolated disputes; it represents a potential restructuring of the programmatic ecosystem. The pressures of declining revenue are forcing a re-evaluation of existing business models and prompting a more aggressive stance in competitive battles.

Key developments and their potential implications:

- The Rise of Integrated Solutions: The move by some DSPs to integrate more directly with supply or build end-to-end solutions suggests a trend towards greater consolidation and control within the advertising supply chain. This could lead to a bifurcation of the market, with large, integrated players competing against more specialized or independent entities.

- Focus on Transparency and Efficiency: The persistent discussions around invalid traffic and the “reseller” designation underscore a growing demand from advertisers and agencies for greater transparency and efficiency in programmatic transactions. Companies that can demonstrably provide clean, high-quality inventory and clear reporting are likely to gain an advantage.

- The Role of Industry Standards: The increasing pressure on organizations like the IAB Tech Lab and Prebid highlights the critical need for robust industry standards and governance. These bodies will play a crucial role in navigating these conflicts, establishing fair practices, and ensuring a level playing field.

- Investor Scrutiny: The heightened investor focus on ad tech earnings signals a period of increased scrutiny. Companies that can demonstrate sustainable revenue growth, operational efficiency, and a clear strategic vision will be better positioned to attract and retain investment. Conversely, those struggling with declining revenues or embroiled in public disputes may face significant challenges.

The current climate is characterized by a complex interplay of financial realities, strategic ambitions, and evolving industry dynamics. The disputes over data access, the definition of roles within the supply chain, and the increasing assertiveness of major players like The Trade Desk are all symptoms of a market under pressure to adapt and evolve. As the industry moves forward, the ability of companies to navigate these challenges with transparency, efficiency, and a clear value proposition will be paramount to their success. The coming quarters will likely reveal which strategies are most effective in this increasingly competitive and dynamic ad tech environment.