Tuesday, November 18th, 2025 – 1:13 pm

The digital advertising technology landscape is in the throes of a significant upheaval, marked by escalating competitive tensions and a dramatic restructuring of relationships between key players. Throughout 2025, a palpable sense of friction has permeated the industry, particularly between demand-side platforms (DSPs) and supply-side platforms (SSPs). This friction is not merely ideological but is directly impacting financial performance, as evidenced by recent earnings reports from prominent ad tech companies. The once-unified front against perceived Google dominance has fractured, replaced by a more complex ecosystem where alliances are shifting, and companies are fiercely guarding their market share and profit margins.

The core of the current discord lies in access to bidstream data and the evolving architecture of programmatic auctions. Companies that had invested heavily in Google’s Chrome Privacy Sandbox initiative now feel sidelined, while dominant players like The Trade Desk are leveraging their market position to reshape industry standards. Industry bodies such as Prebid.org and the IAB Tech Lab are finding themselves at the center of these disputes, tasked with navigating the competing interests of various stakeholders. These internal industry battles are no longer confined to technical discussions; they are manifesting in tangible financial results and strategic maneuvers that are reshaping the future of programmatic advertising.

The Financial Fallout: Declining Revenues and Shifting Spend

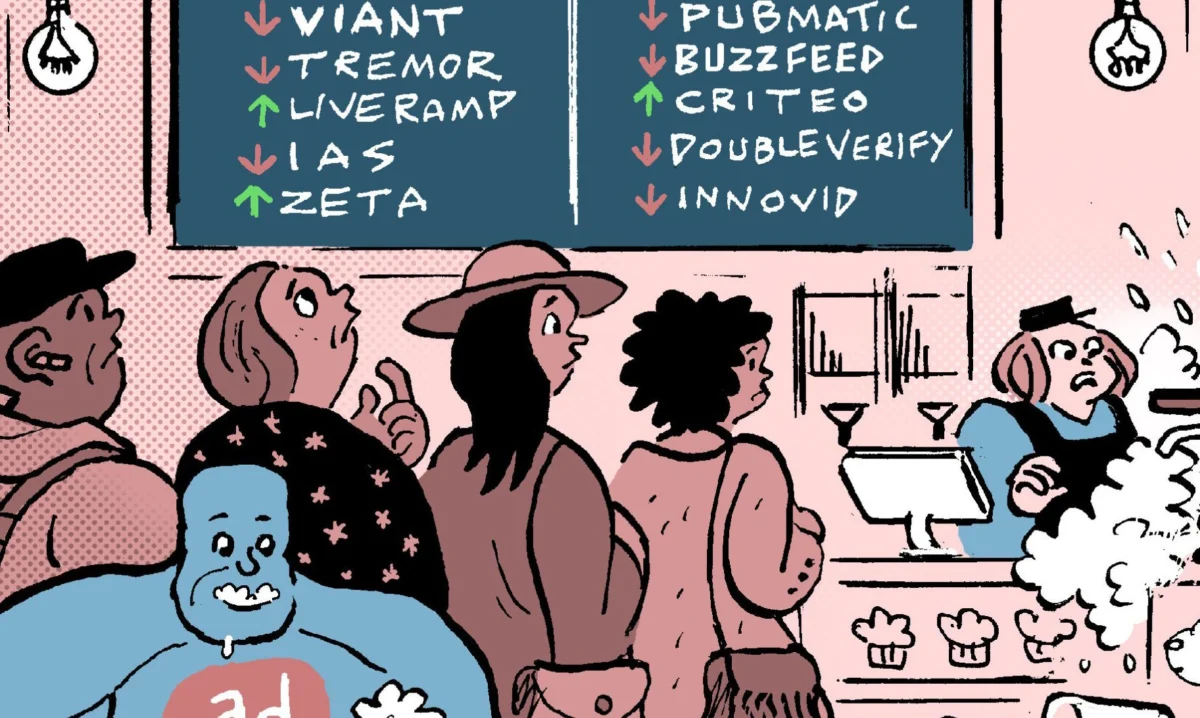

The most concrete indicator of the brewing storm is the significant decline in revenue reported by several key ad tech firms in the third quarter of 2025. Magnite, PubMatic, and Nexxen, all prominent SSPs, have disclosed unexpected and precipitous decreases in spending from unnamed DSPs, or potentially a single dominant DSP, on their platforms. This abrupt retraction of ad spend has sent ripples of concern through the investor community, prompting a reevaluation of the industry’s stability and growth prospects.

PubMatic CEO Rajeev Goel, while not directly naming The Trade Desk, alluded to the impact of their new ad-buying platform, Kokai. He characterized Kokai’s operational approach as "differently from what we have seen," echoing sentiments previously expressed by PubMatic’s leadership regarding a sudden reduction in spend from a specific DSP. This subtle yet pointed observation suggests that changes implemented by The Trade Desk are directly influencing the flow of advertising budgets.

Magnite’s CEO, Michael Barrett, was more direct in his commentary during the company’s quarterly earnings call. He explicitly stated that The Trade Desk had implemented a change that "prioritized OpenPath as a default path for supply." This strategic shift by The Trade Desk, a major source of demand in the programmatic ecosystem, forced SSPs like Magnite to engage directly with major agency buyers to re-establish "preferred supply paths." Barrett acknowledged the significant impact of this change, given the symbiotic relationship between The Trade Desk’s demand and Magnite’s supply.

Nexxen, which operates both a DSP and an SSP, revised its financial forecast downwards for the remainder of the year. CEO Ofer Druker cited a lack of the anticipated seasonal growth surge in October, a period typically characterized by increased advertising activity leading into the holiday season. Druker indicated that this was not an isolated incident with a single DSP but rather a programmatic-wide reduction plateau that failed to materialize. This suggests a broader systemic issue impacting revenue streams across the industry.

Further compounding the revenue concerns, System1 CEO Michael Blend reported that an unnamed programmatic vendor in their demand channel had exposed the company to "significant invalid or nonhuman" traffic. System1 is actively seeking reimbursement for these fraudulent impressions and is considering legal action, highlighting the persistent problem of ad fraud and its financial repercussions.

Strategic Maneuvering: Redefining Roles and Architectures

Beyond the immediate financial pressures, the increased antagonism in the programmatic space is also a manifestation of companies strategically positioning themselves and vying for investor and marketer confidence. Each player is attempting to frame the narrative around how programmatic advertising should operate, often in direct opposition to their rivals.

The Trade Desk CEO Jeff Green, for instance, has publicly questioned the classification of Amazon’s offerings, stating, "I don’t think Amazon has a DSP as we define it." This statement implicitly challenges the competitive landscape and seeks to delineate a specific category of buy-side platforms, potentially to highlight The Trade Desk’s perceived purity of purpose.

Conversely, Viant, a smaller independent DSP, frames the competitive environment differently. CEO Tim Vanderhook asserts that Viant faces "less competition when you look at truly objective buy-side-only platforms." This framing strategically excludes The Trade Desk from this category, characterizing it as "no longer independent or objective" due to its preference for its own OpenPath supply integrations. This highlights the growing trend of DSPs integrating more directly with supply, blurring the lines between the two sides of the advertising transaction.

Nexxen’s CEO, Ofer Druker, also weighed in on this trend, noting that "Big DSPs in the future will have to build their own end-to-end solutions in order to increase their margins." This perspective suggests a future where DSPs are increasingly vertically integrated, controlling more of the supply chain to capture greater revenue. This contradicts the traditional model where DSPs and SSPs operated more distinctly.

These divergent viewpoints underscore the fundamental disagreements about the structure and future of programmatic advertising. The classification of players, particularly the designation of SSPs as "resellers" by entities like The Trade Desk, has become a contentious point.

The "Reseller" Debate and Ecosystem Complexity

The classification of SSPs as "resellers" has ignited significant concern among investors. This label, often implying a less direct or value-added role in the supply chain, can negatively impact perceptions of an SSP’s importance and profitability.

PubMatic CEO Rajeev Goel has vehemently denied that his company fits this description. He emphasized that PubMatic is a "strong partner of The Trade Desk’s" and is not a reseller. Goel, while acknowledging the decrease in spend from The Trade Desk, downplayed its significance, referring to the "reseller noise that’s out there" as a distraction from the broader, complex nature of the ecosystem. He characterized the industry as "multifaceted, certainly complex."

Magnite’s Michael Barrett echoed this sentiment, asserting that while the problem of supply-side resellers is real, it does not apply to Magnite. He expressed Magnite’s commitment to "cleaning up the system" by eliminating duplicate bids and low-quality impressions, positioning the company as a facilitator of a healthier ad ecosystem. Barrett clearly stated, "we don’t believe Magnite is a reseller. I think the term applies to others."

This debate over the "reseller" designation highlights a broader struggle for control and influence within the programmatic supply chain. SSPs are keen to emphasize their direct relationships with publishers and their role in optimizing ad delivery, pushing back against any attempts to relegate them to intermediary status.

Underlying Causes and Future Implications

The heated rhetoric and strategic maneuvers are not merely about philosophical stances on data transparency or supply chain roles. The fundamental driver appears to be economic pressure. As advertising budgets tighten and the cost of acquiring and retaining customers rises, every player in the ecosystem is feeling the pinch.

The shift towards more direct integrations, exemplified by The Trade Desk’s OpenPath initiative, is an attempt to reduce intermediaries and potentially capture a larger share of the advertising dollar. For SSPs, this means facing increased competition not only from other SSPs but also from DSPs that are increasingly controlling their own supply paths.

The implications of these ongoing battles are far-reaching. The industry is witnessing a potential consolidation of power, with dominant platforms like The Trade Desk exerting significant influence over the flow of advertising spend. This could lead to a less diverse and more concentrated programmatic ecosystem, raising concerns about fairness and innovation.

Furthermore, the increased scrutiny on ad tech performance, including the prevalence of invalid traffic and the efficiency of ad spend, is likely to intensify. Marketers and agencies will demand greater transparency and accountability from all parties involved.

The evolution of privacy-centric technologies, such as Google’s Privacy Sandbox, continues to add another layer of complexity. Companies that had bet heavily on specific approaches are now re-evaluating their strategies as the landscape shifts.

In conclusion, the ad tech industry is at a critical juncture. The year 2025 has been characterized by intensifying competition, financial pressures, and strategic repositioning. The relationships between DSPs and SSPs are being redefined, and the very architecture of programmatic advertising is undergoing a significant transformation. The outcome of these ongoing battles will shape the future of digital advertising, influencing how brands reach consumers and how publishers monetize their content for years to come. The coming months will likely see further strategic moves, potential alliances, and continued scrutiny as the industry grapples with these fundamental shifts.