The digital commerce landscape is currently undergoing a fundamental shift as artificial intelligence and social media platforms attempt to centralize the shopping experience, yet new consumer data suggests that direct-to-consumer brand websites maintain a significant, albeit fragile, advantage in the marketplace. While the narrative surrounding ecommerce often frames AI as an immediate existential threat to independent retailers, a nuanced analysis of shopper behavior reveals that trust, security, and emotional connection remain the primary drivers of direct sales. However, this “trust moat” is facing unprecedented pressure as platforms like Google, Meta, and OpenAI refine their commerce capabilities to bridge the gap between discovery and transaction.

The Persistence of the Direct-to-Consumer Model

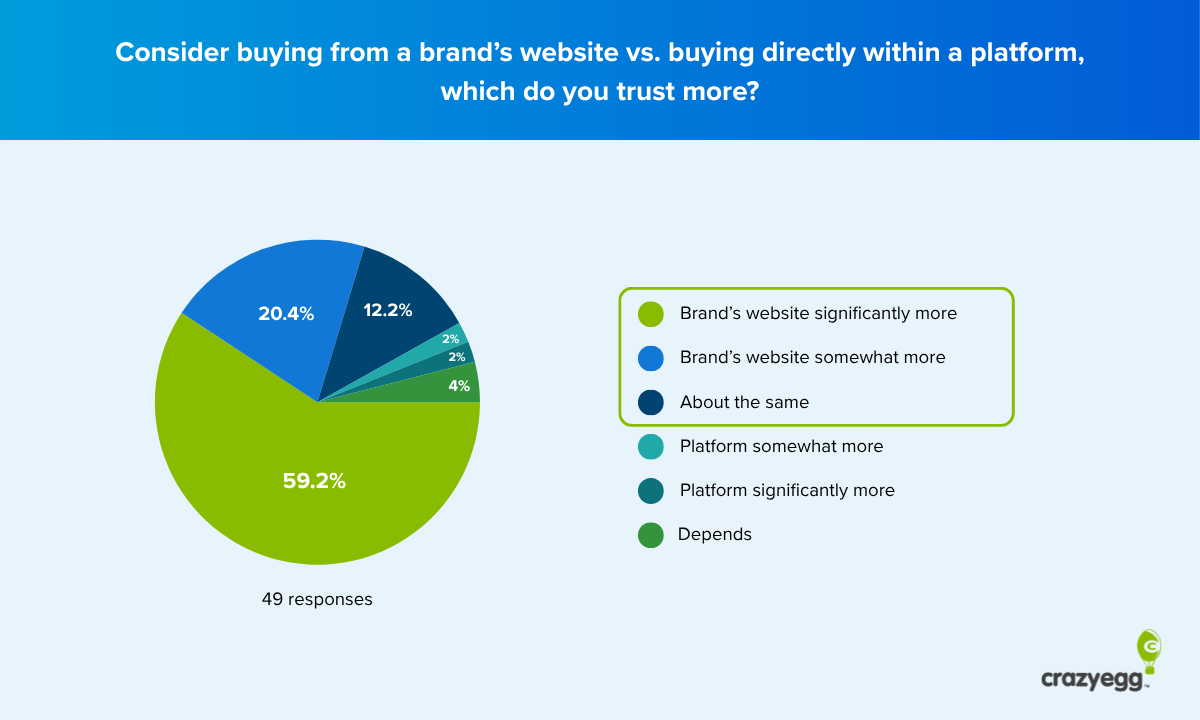

Despite the convenience offered by “one-click” shopping within social media apps and AI interfaces, recent survey data indicates that a majority of online shoppers still prefer to conduct transactions directly on a brand’s official website. This preference is not necessarily rooted in a superior user interface or better pricing, but rather in a deep-seated skepticism toward the third-party platforms that facilitate the initial product discovery.

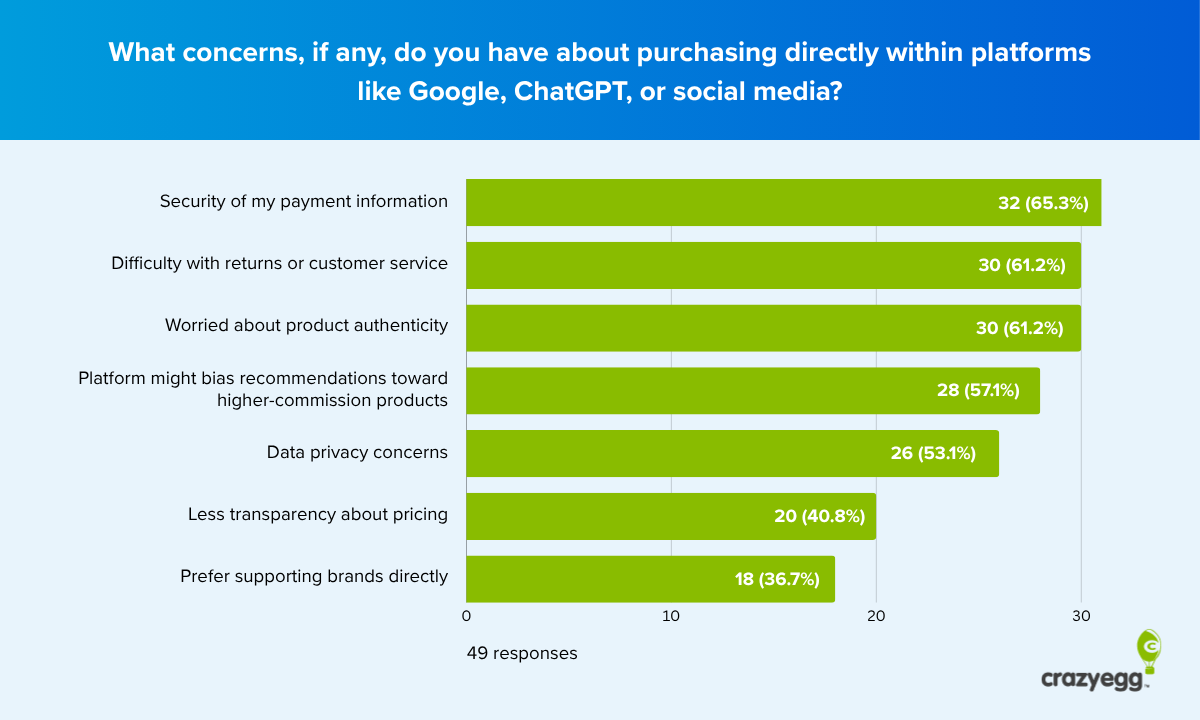

According to research conducted by Crazy Egg involving a targeted group of online shoppers, the primary reason consumers bypass the convenience of platform-based shopping is a lack of trust in the alternative systems. Specifically, 65% of respondents cited payment security as their top concern when considering a purchase through an AI tool or social media platform. Furthermore, 61% expressed apprehension regarding the difficulty of managing returns or accessing customer service through these intermediaries, and another 61% voiced concerns about product authenticity.

These findings suggest that for the time being, independent ecommerce brands are protected by a defensive barrier of reliability. While platforms like TikTok and Instagram have successfully integrated “Shop” features, and ChatGPT briefly experimented with “Instant Shopping” before scaling back, the consumer psyche remains tethered to the perceived safety of the brand’s own digital storefront.

A Chronology of Digital Commerce Evolution

To understand the current tension between brands and platforms, it is necessary to examine the evolution of the online shopping journey over the last decade.

- The Direct-to-Consumer (DTC) Boom (2010–2018): Brands like Warby Parker and Allbirds pioneered a model that bypassed traditional retailers, focusing on building direct relationships with consumers via proprietary websites. Trust was built through high-quality storytelling and controlled fulfillment.

- The Marketplace Dominance (2014–Present): Amazon’s rise forced brands to choose between the reach of a massive marketplace and the control of a direct site. This era established the “convenience vs. connection” trade-off.

- The Social Commerce Wave (2019–2022): Instagram and TikTok introduced native checkout features, attempting to shorten the funnel from discovery to purchase. However, consumer adoption was slowed by concerns over data privacy and “drop-shipping” scams.

- The AI Integration Era (2023–Present): The emergence of Large Language Models (LLMs) like ChatGPT and Google’s Gemini introduced the concept of “AI-assisted shopping,” where an algorithm recommends and potentially purchases items on behalf of the user.

While the timeline suggests an inevitable move toward platform-centric shopping, the failure of various “instant checkout” initiatives—such as OpenAI’s recent pivot away from direct commerce integration—highlights the persistent technical and psychological hurdles that remain.

Analyzing the Trust Moat: Security and Authenticity

The data reveals that the “trust moat” is constructed from three specific pillars: payment security, customer service reliability, and product authenticity. For ecommerce brands, these are not merely operational requirements but strategic assets.

Industry analysts note that when a consumer visits a brand’s website, they are looking for “trust signals” that platforms have yet to perfect. These include clear return policies, visible contact information, and verified customer reviews that feel organic rather than algorithmic. The survey data supports this, showing that shoppers feel a sense of “uncomfortability” (currently cited by 71% of respondents) when asked to enter payment details into an AI interface or a social media sidebar.

However, this advantage is not permanent. Platforms are aggressively working to implement verified seller badges, end-to-end encryption for payments, and centralized return processing. As these features become standard, the “trust tax” that consumers are currently willing to pay to shop direct will likely decrease.

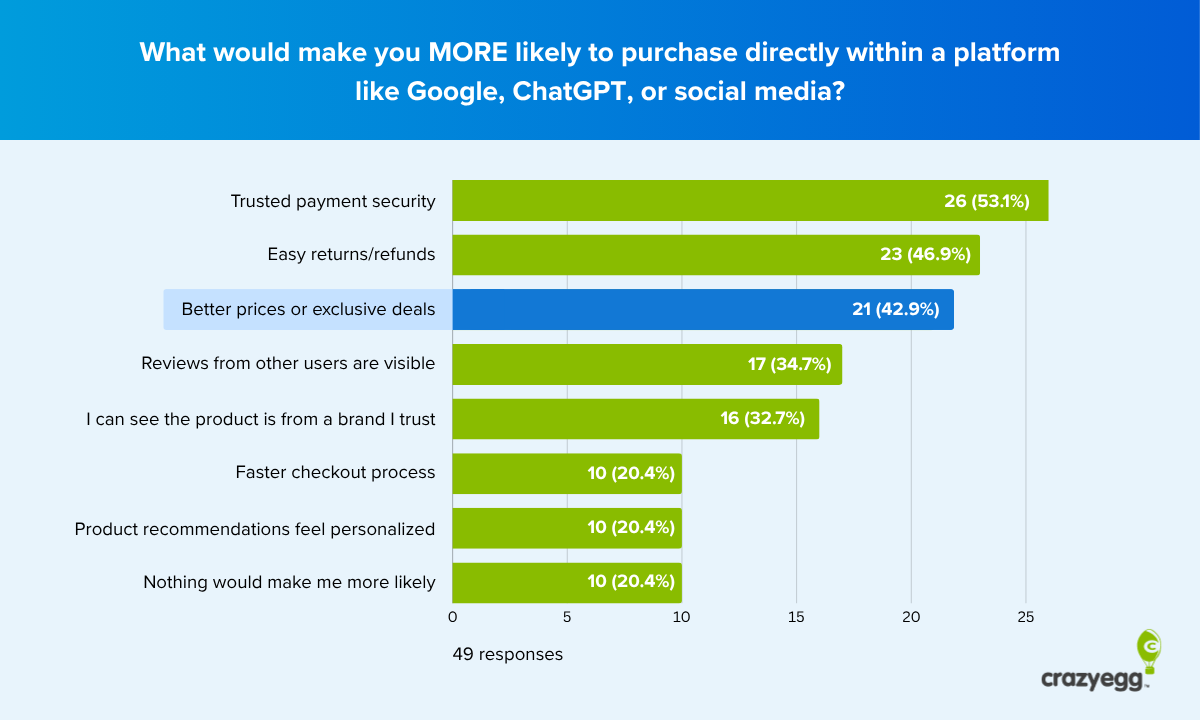

The Value Vulnerability: Bridging the Pricing Divide

Perhaps the most significant risk to the DTC model is the perceived “value gap.” The research indicates that brand websites are often viewed as more expensive than marketplaces or platform-driven deals. Only 51% of shoppers who prefer buying direct believe they are getting the best possible value.

Open-text responses from the survey highlight a growing frustration: many consumers believe that the Manufacturer’s Suggested Retail Price (MSRP) is almost always higher on the brand’s own site compared to what might be found via a platform search or a marketplace discount. Currently, 42.9% of shoppers admitted they would be more likely to switch to in-platform shopping if they were offered a significantly better deal.

This suggests that loyalty is often conditional. If a platform can provide the same product with better security and a lower price, the brand’s direct relationship may not be enough to prevent churn. To counter this, successful brands are shifting their focus toward “exclusive value”—offering loyalty points, early access to new products, or bundled services that cannot be replicated by a third-party algorithm.

Case Study: The Post-Purchase Emotional Connection

One of the most potent ways brands are maintaining their direct relationships is through the post-purchase experience. While a platform transaction is often cold and functional, a direct transaction allows for emotional storytelling.

Freshly Cosmetics, a natural skincare brand, serves as a primary example of this strategy. By moving away from generic automated emails and implementing a sophisticated post-purchase flow, the brand was able to see a 136% increase in revenue from repeat customers. Their strategy involved:

- Educational Content: Sending emails that explain exactly how to use a product to see the best results.

- Value Alignment: Reminding the customer of the brand’s ethical and environmental standards immediately after the sale.

- Milestone Recognition: Celebrating the customer’s journey with the brand.

This level of personalization is currently impossible for AI platforms to achieve at scale. The emotional “high” of buying from a brand that shares one’s values remains a unique selling proposition for the DTC model.

The AI Shift: From Search Engines to Answer Engines

As we look toward the future, the nature of product discovery is changing. Traditional Search Engine Optimization (SEO) is being supplanted by Generative Engine Optimization (GEO). When a consumer asks an AI tool, “What is the best waterproof hiking boot for wide feet?” the AI does not provide a list of links; it provides a definitive recommendation.

For ecommerce brands, the risk is becoming “invisible” at the point of consideration. If a brand’s data is not structured in a way that AI models can digest, that brand will never appear in the AI’s shortlist. This creates a two-pronged challenge: brands must optimize their own stores for trust and conversion, but they must also ensure their product data is “discoverable” by the very platforms they are competing against.

Industry experts suggest that brands should focus on:

- Schema Markup: Using technical code to tell search engines exactly what a product is, its price, and its availability.

- Brand Authority: Ensuring the brand is mentioned in high-quality, third-party publications that AI models use as training data.

- Platform Presence: Maintaining a presence on social commerce platforms to ensure the brand remains in the “consideration set,” even if the final transaction happens on the brand’s website.

Broader Impact and Strategic Implications

The broader implication of this data is that the “loyalty” consumers feel toward brands is more fragile than previously thought. The survey revealed a startling trend: once a consumer makes even one successful purchase within a platform, their resistance to platform-based shopping drops precipitously.

Those who have bought “in-platform” are significantly more likely to trust AI recommendations (46% vs. 15% for those who haven’t) and are much more likely to believe that platforms offer better value than brand websites. This suggests that the “first purchase” on a platform is the ultimate barrier. Once that barrier is breached, the brand’s direct-to-consumer moat begins to evaporate.

In conclusion, the window of opportunity for ecommerce brands to solidify their direct relationships is currently open, but it is narrowing. To survive the next decade of AI-driven commerce, brands cannot rely solely on the fact that they have a website. They must actively optimize for trust signals, aggressively close the value gap through loyalty programs, and leverage the post-purchase window to build an emotional connection that an algorithm cannot replicate. The winner in the age of AI will not be the brand with the best technology, but the brand that remains the most “human” in an increasingly automated marketplace.