Tuesday, November 18th, 2025 – 1:13 pm

The digital advertising technology (ad tech) landscape is experiencing a period of intense upheaval, characterized by escalating competitive tensions, strategic maneuvering, and a tangible impact on company revenues. A year marked by ongoing debates over data access, the evolving privacy landscape, and the strategic decisions of major industry players has culminated in a critical juncture, as evidenced by recent earnings reports from prominent ad tech firms. The previously unified front against perceived dominance by tech giants has fractured, replaced by internal friction and a desperate scramble for market share and profitability.

The Shifting Sands of Programmatic Advertising

For years, many independent programmatic advertising companies found common ground in their collective reliance on Google’s ecosystem and their shared concerns about its market power. This era of relatively cohesive opposition has dissolved, replaced by a more complex and often adversarial dynamic. The current animosity within the programmatic space, while often framed in terms of philosophical disagreements about data transparency or supply chain roles, is fundamentally driven by a stark reality: reduced financial performance across the board.

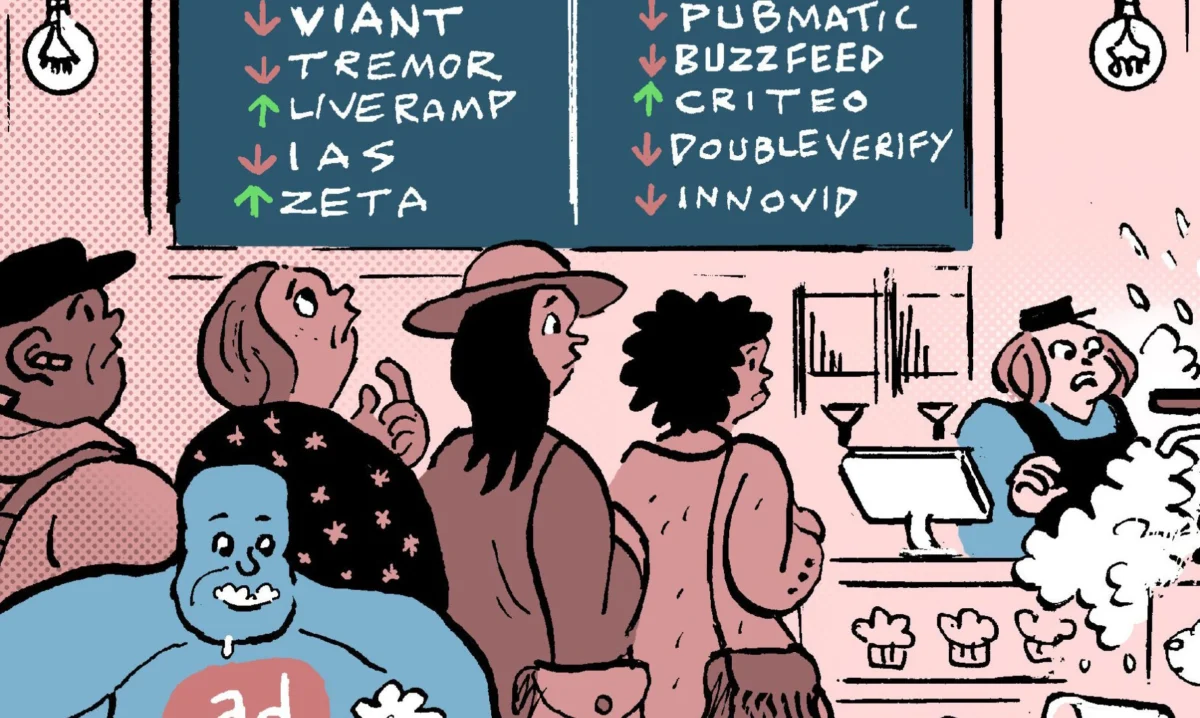

This downturn is manifesting in concrete ways for key industry participants. Magnite, PubMatic, and Nexxen, prominent Supply-Side Platforms (SSPs) and integrated ad tech providers, have all reported significant and unexpected decreases in spending from Demand-Side Platforms (DSPs) during the third quarter of 2025. These reductions have directly impacted their financial results, prompting a reassessment of market strategies and client relationships.

The Trade Desk’s Strategic Moves and Their Ripple Effects

A recurring theme in these earnings calls is the strategic repositioning undertaken by The Trade Desk (TTD), a leading independent DSP. PubMatic CEO Rajeev Goel alluded to TTD’s new ad-buying platform, Kokai, noting that its operational methodology differs from previous approaches. This statement echoes earlier characterizations of a sudden spending decrease from a specific DSP that PubMatic leadership had previously discussed.

More explicitly, Magnite CEO Michael Barrett directly attributed a portion of their Q3 revenue dip to a decision by The Trade Desk. Barrett stated that TTD had implemented a change that "prioritized OpenPath as a default path for supply." OpenPath is TTD’s initiative to create more direct pathways between buyers and sellers of ad inventory, aiming to reduce intermediaries and enhance efficiency. However, this strategic shift appears to have bypassed traditional SSPs like Magnite, forcing them to engage directly with major agency buyers to re-establish preferred supply arrangements. Given TTD’s substantial role as a demand aggregator and Magnite’s position as a significant source of programmatic supply, this recalibration inevitably had a material impact on Magnite’s revenue.

Nexxen, which operates both a DSP and an SSP, also experienced a slowdown. CEO Ofer Druker cited a failure to anticipate the typical Q4 surge in programmatic advertising spending. He indicated that the reduction was not isolated to a single DSP but represented a broader programmatic plateau that failed to materialize before the crucial holiday season. Druker’s analysis suggests a systemic issue rather than a targeted disruption, though the underlying causes remain a subject of intense debate.

Broader Market Pressures and Allegations of Malfeasance

Beyond the direct impact of DSP spending shifts, the ad tech ecosystem is grappling with other significant challenges. System1 CEO Michael Blend disclosed that the company had been subjected to "significant invalid or nonhuman" traffic from an unnamed programmatic vendor within its demand channel. This situation has led System1 to seek reimbursements and consider legal action, highlighting ongoing concerns about ad fraud and the integrity of the programmatic supply chain. Such incidents further erode advertiser confidence and can lead to broader reductions in ad spend as marketers become more risk-averse.

The Strategic Battle for Narrative Control

While companies are undeniably focused on their immediate financial performance, the heightened antagonism within the ad tech sector also represents a strategic effort to influence investor perception and shape the narrative around the future of programmatic advertising. Each player is attempting to frame the ongoing changes in a way that benefits their long-term positioning.

The Trade Desk CEO Jeff Green, for instance, has publicly questioned the operational definition of Amazon’s advertising business, suggesting it doesn’t fit the traditional DSP model. This subtle distinction could be aimed at differentiating TTD’s platform and influencing how market analysts and investors categorize its competitors.

In parallel, Viant, an independent DSP, is actively crafting its competitive landscape. CEO Tim Vanderhook stated that Viant perceives less competition when focusing on "truly objective buy-side-only platforms." This framing strategically excludes The Trade Desk, which Vanderhook characterized as "no longer independent or objective" due to its preferential treatment of its OpenPath supply integrations. This highlights a growing divide between DSPs that advocate for open, neutral marketplaces and those that are integrating more directly with supply sources to gain a competitive edge.

Nexxen’s Druker offered a broader industry perspective, predicting that "Big DSPs in the future will have to build their own end-to-end solutions in order to increase their margins." This forecast suggests a trend towards vertical integration, where major demand-side players may increasingly seek to control more of the advertising supply chain to improve profitability and reduce reliance on third-party platforms. The conflicting viewpoints expressed by these independent DSPs underscore the fundamental disagreements about the ideal structure and operation of the modern programmatic ecosystem.

The "Reseller" Debate and SSPs’ Defense

The designation of certain SSPs as "resellers" by The Trade Desk has become a point of contention among investors. This label implies a layer of intermediation that could be seen as adding cost and reducing efficiency. However, leading SSPs are actively pushing back against this categorization.

PubMatic’s Rajeev Goel asserted that his company is not a reseller and emphasized its strong partnership with The Trade Desk. He downplayed the significance of the reduced spending and the "reseller noise," framing the ecosystem as inherently "multifaceted" and "complex." This suggests a strategic effort to retain TTD as a partner while mitigating any negative investor sentiment associated with the "reseller" label.

Magnite’s Michael Barrett echoed this sentiment, agreeing that supply-side resellers present a genuine problem but insisted that it does not apply to Magnite. He expressed support for initiatives aimed at "cleaning up the system" by eliminating duplicate bids and low-quality impressions. Barrett’s clear statement, "we don’t believe Magnite is a reseller," indicates a firm stance against being lumped in with entities perceived as adding less value to the programmatic chain.

The Broader Implications for the Ad Tech Ecosystem

The current turbulence in ad tech is more than just a temporary financial blip; it signals a fundamental recalibration of the industry’s power dynamics and operational models. The move towards more direct relationships, exemplified by The Trade Desk’s OpenPath, reflects a broader industry trend of disintermediation and a quest for greater efficiency and transparency.

For advertisers and brands, this period of flux presents both challenges and opportunities. Increased competition among platforms could lead to more favorable pricing and improved campaign performance. However, the fragmentation and strategic maneuvering also raise concerns about the complexity of the supply chain and the potential for opaque practices. Advertisers will need to be more vigilant in understanding where their ad spend is going and the value derived from each intermediary.

The ongoing evolution of privacy regulations, particularly concerning third-party cookies and data tracking, continues to be a significant backdrop to these developments. Companies that can successfully navigate the privacy landscape while demonstrating clear value and transparency are likely to emerge stronger from this period of disruption. The ad tech industry is at a critical crossroads, and the decisions made by key players in the coming months will undoubtedly shape its future trajectory for years to come. The focus will likely remain on demonstrating measurable ROI, maintaining supply chain integrity, and adapting to an increasingly privacy-conscious digital advertising environment.