The global e-commerce landscape is currently navigating a pivotal transition as the traditional relationship between brands and consumers faces increasing pressure from artificial intelligence and consolidated tech platforms. For years, the conversation regarding AI in retail has been framed as an existential threat to direct-to-consumer (D2C) brands, suggesting that automated shopping assistants and social media marketplaces would eventually render brand-owned websites obsolete. However, recent market data and consumer sentiment analysis reveal a more nuanced reality: while big tech platforms like Google, Amazon, and TikTok are encroaching on the sales funnel, brand websites currently maintain a significant "trust moat" that offers a critical, albeit narrowing, window of opportunity for independent retailers.

The Current State of Consumer Trust and Platform Encroachment

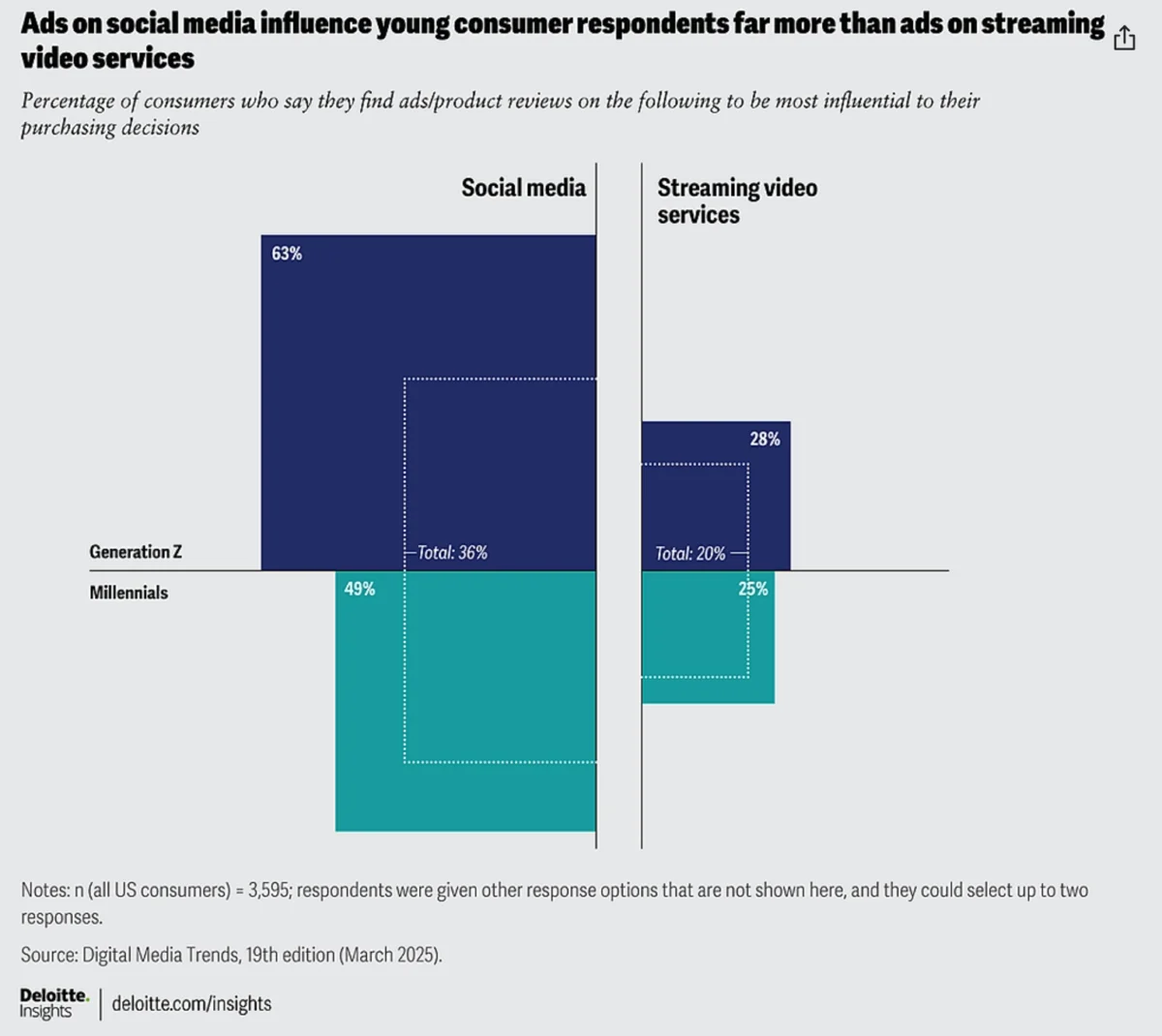

Recent survey data involving a cross-section of online shoppers indicates that the perceived dominance of big tech in the final purchase stage may be premature. Despite the massive investments by companies like OpenAI and Meta to integrate shopping directly into their interfaces, a substantial majority of consumers still express a strong preference for purchasing directly from a brand’s official website. This preference is not necessarily rooted in a superior user interface or better pricing, but rather in a deep-seated distrust of third-party platforms when it comes to the final transaction.

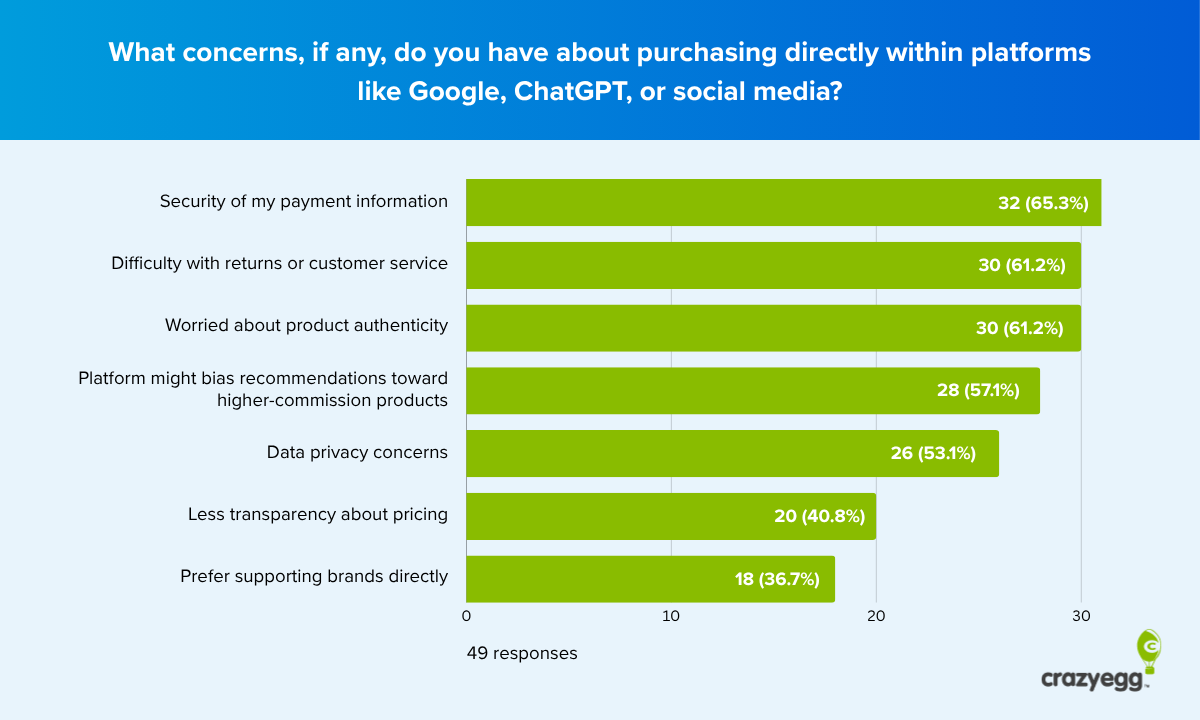

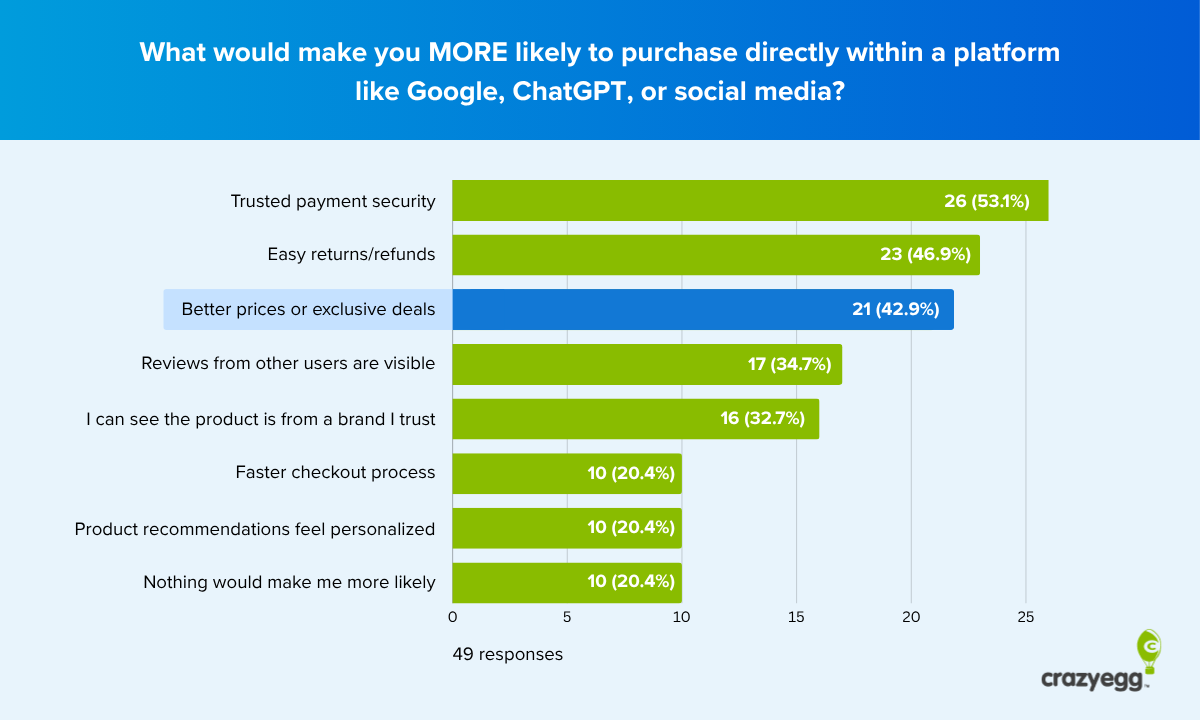

According to the data, 71% of shoppers currently report feeling uncomfortable making purchases directly within a platform such as ChatGPT, TikTok, or Google. This discomfort stems from three primary concerns: payment security, cited by 65% of respondents; the perceived difficulty of managing returns or accessing customer service through a third party (61%); and anxieties regarding product authenticity (61%). For D2C brands, these factors represent a defensive barrier. As long as big tech platforms struggle to provide the same level of perceived security and post-purchase accountability as a direct brand site, the direct sales channel remains viable.

Chronology of the Shift Toward AI-Assisted Commerce

The evolution of the digital storefront has moved through several distinct phases over the last decade, leading to the current friction between brands and platforms:

- The Era of Search Dominance (2010–2018): Brands relied heavily on Search Engine Optimization (SEO) and Search Engine Marketing (SEM) to drive traffic to their websites. The platform (Google) acted as a middleman that directed users elsewhere.

- The Rise of Social Commerce (2019–2022): Platforms like Instagram and TikTok began introducing "Shop" features, attempting to keep the user within their ecosystem. While discovery thrived, conversion often still occurred on the brand’s site due to trust issues.

- The AI Integration Phase (2023–Present): With the explosion of Large Language Models (LLMs), platforms began experimenting with "Instant Shopping." However, this phase has seen setbacks; for instance, ChatGPT recently scaled back its Instant Checkout features as it realized the complexities of logistics and consumer trust.

- The Discovery Shift (2024 and Beyond): We are now entering a period where AI tools are taking over the research and discovery phase. Even if the purchase happens on a brand site, the "consideration set"—the list of brands a consumer even thinks about—is being curated by AI before the consumer ever types a URL.

Analysis of the Trust Moat: Why Consumers Stay

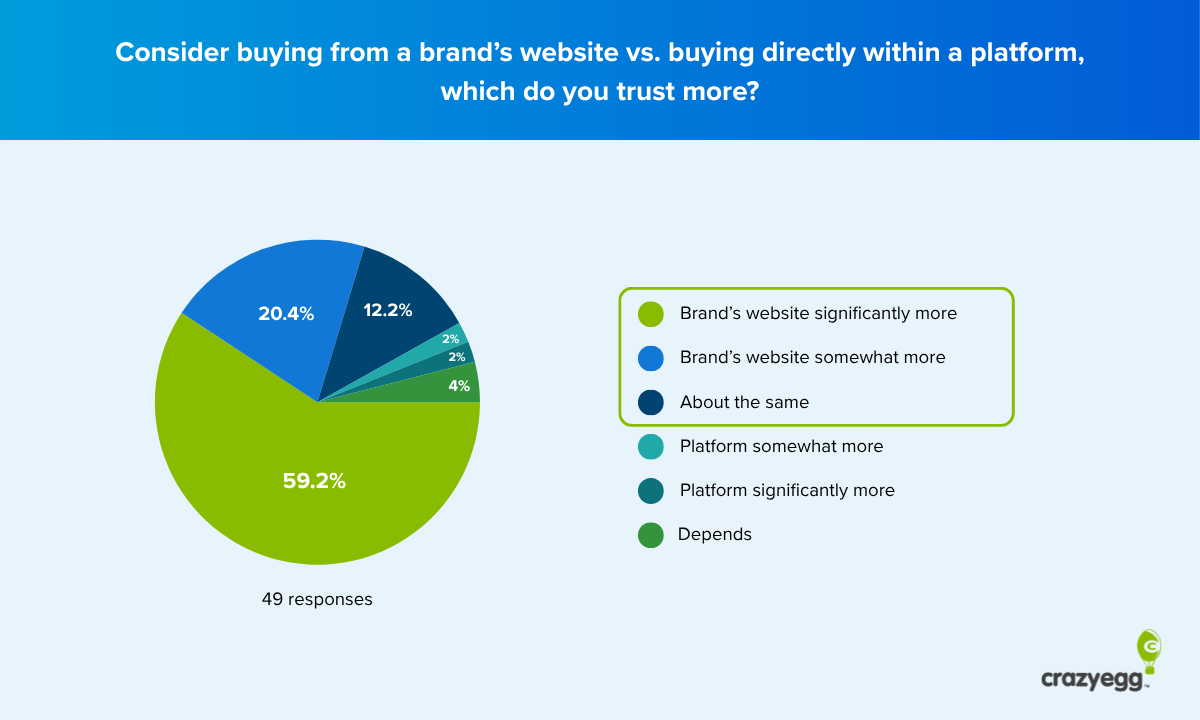

The trust advantage held by brand websites is currently doing the heavy lifting for direct sales. In many cases, shoppers are choosing to buy direct even when they suspect they might be paying a higher price. This phenomenon, often referred to as a "trust tax," suggests that consumers are willing to pay for the peace of mind that comes with a direct relationship.

However, industry analysts warn that this moat is fragile. "Trust is currently a significant defensive moat for e-commerce brands," the report notes, "but platforms will get better at trust signals." Tech giants are already iterating on verified seller badges, ironclad return guarantees, and biometric-secured checkout flows. When a platform like Google or Amazon can guarantee a return as easily as an independent brand can, the primary reason for buying direct could vanish overnight.

To maintain their lead, brands must move beyond basic security and optimize for "active trust." This includes making trust signals visible throughout the journey—not just at checkout. Factors such as clear shipping timelines, visible "About Us" stories that humanize the company, and easily accessible customer service contact information are no longer optional; they are the primary tools for customer retention.

The Value Gap: A Growing Vulnerability

While trust favors the brands, "value" favors the platforms. The survey data reveals a concerning trend for D2C retailers: only 51% of shoppers who prefer brand websites believe they are getting a better deal by buying direct. The remaining 49% either believe they are paying more or are unsure. Open-text responses from consumers highlight a prevailing sentiment that Manufacturer’s Suggested Retail Prices (MSRP) are almost always higher on a brand’s own site than on a marketplace like Amazon or a discount-heavy platform.

Furthermore, 42.9% of shoppers indicated they would be willing to overcome their discomfort with in-platform shopping if they were offered a significantly better price or an exclusive discount. This suggests that price elasticity is a major threat to brand loyalty. If a platform can offer a 20% discount through an AI-assistant-led promotion, nearly half of the "loyal" direct shoppers might migrate.

To close this gap, brands are being encouraged to rethink their value proposition. If they cannot compete on raw price, they must offer "platform-exclusive" value on their own sites. This might include:

- Exclusive Product Access: Items that are not listed on marketplaces.

- Loyalty Programs: Points or rewards that can only be redeemed through the direct channel.

- Bundled Services: Free extended warranties or personalized consultations for direct buyers.

The Role of Post-Purchase Connection

One area where big tech platforms structurally struggle to compete is the emotional connection formed after a sale. The data shows that 59% of respondents feel more connected to a brand when buying from its website directly. Among those who have never made an in-platform purchase, this number jumps to 69%.

Professional analysis of successful D2C brands, such as Freshly Cosmetics, demonstrates the power of the post-purchase phase. Instead of treating the order confirmation as the end of the transaction, successful brands use it as the beginning of a relationship. Freshly Cosmetics, for example, implemented a post-purchase email flow that tailored content based on whether the customer was a first-time or repeat buyer. By providing educational content on how to use products and highlighting brand values, they saw a 136% increase in revenue from repeat customers.

This "brand connection" is a strategic asset. While an AI assistant can facilitate a transaction, it cannot easily replicate the feeling of belonging to a community or supporting a brand with shared values.

The Rapid Shift in Loyalty

Perhaps the most startling finding in the recent data is how quickly consumer behavior changes after a single successful in-platform purchase. The survey suggests that making just one purchase via a social media shop or an AI interface acts as a "gateway."

Shoppers who have bought in-platform even once are:

- Significantly more likely to trust platforms for future purchases.

- More likely to believe platforms offer better value than brand sites.

- Less likely to feel a meaningful connection to the brands they buy from.

This indicates that the barrier to entry for platforms is "familiarity." Once the initial hurdle of the first transaction is cleared, the "trust moat" of the brand website evaporates rapidly. This puts immense pressure on brands to ensure that the first time a customer discovers them, they are incentivized to buy direct, preventing that first platform transaction from occurring.

Broader Impact and Strategic Implications for AI Discovery

As we look toward 2025, the challenge for e-commerce brands is twofold: they must protect their direct relationships while simultaneously preparing for a world where AI is the primary gatekeeper of discovery.

For brands that are "relationship-led"—those selling high-end, luxury, or values-based goods—the priority remains the direct channel. These brands may even choose to avoid marketplaces to protect their brand equity. However, for "product-led" brands—those selling commodities or price-competitive goods—omnipresence is the only path forward.

For the latter, optimizing for AI visibility is becoming as important as traditional SEO. This involves:

- Structured Data: Ensuring that website code (Schema markup) is flawlessly organized so AI crawlers can accurately read product details, pricing, and availability.

- Brand Authority: Building a footprint of reviews and mentions across the web so that when an AI tool like Perplexity or ChatGPT is asked for a recommendation, the brand appears in the generated "shortlist."

- Platform Participation: Recognizing that if a competitor’s product is shoppable within an AI interface and yours is not, the AI will naturally route the user toward the path of least resistance.

Conclusion: The Hybrid Path to Success

The future of e-commerce will likely not be a total victory for platforms or a total defense for brands, but a hybrid landscape. The brands that thrive will be those that manage to be found everywhere—appearing in AI recommendations and social feeds—while providing a compelling, value-added reason for customers to complete their journey on the brand’s own digital property.

The "trust moat" is a gift of time. It provides a window for brands to harden their infrastructure, deepen their customer relationships, and clarify their value propositions. However, as AI interfaces become more sophisticated and consumer discomfort fades, the brands that rely solely on "the way things have always been" will find themselves invisible in the new age of assisted shopping. The current data serves as a clear call to action: optimize for trust today, or prepare for irrelevance tomorrow.